Money talks

If you want to find out what’s really going on in the alternative proteins sector, you need to talk with the people splashing the cash. Nick Bradley meets 10 leading players from the investment community who know what it takes for start-ups to succeed

There are many factors underlying the alternative proteins market. Whether you are a consumer motivated by having a more sustainable footprint, personal health choices, perhaps concerns about animal welfare, or are just looking for a way to reduce your expenditure, these drivers and many more are impacting our food consumption choices.

The alternative proteins market is also impacted by choices made by farmers growing crops, governments subsidizing the dairy and agricultural sector, governments developing plans to improve food security, and the overall health of their citizens.

There are challenges abound. But alternative proteins and other novel food-tech solutions can significantly contribute to resolving the myriad problems we see today, from climate change and food security to supply chain shocks and the cost-of-living crisis, by making quality protein cheaper and more readily available, and by moving the end-to-end production process closer to local communities.

Here, we gage the state of the sector by speaking with the people who are largely responsible for driving it forward – the investors and accelerators taking ideas from seed to shelf. We compare the boom years of 2020 and 2021 with an entirely different 2022. We find out what it takes to be a successful start-up. We get them to separate the fact from the fiction in the alternative proteins sphere. We discuss the risks and the rewards. And we learn from them where the industry could be heading in the years ahead, as we approach 2050 and a population of ~10 billion people…

Disruptive innovations are needed to secure protein availability

Eatable Adventures is officially an ‘accelerator’. According to José Luis Cabañero, CEO & Co-founder, that makes it a “special type of venture capital vehicle” for start-ups.

The company’s model is based on “identifying the right technologies that will make a dent in the food system”, the Spaniard says, and making sure start-ups have the right team in place to help them reach market. “We support start-ups throughout the entire process from the initial idea of the project until it reaches the market with a training plan, mentoring sessions, and a network of private and public corporate partners so that they can scale their technologies in the most successful way possible.”

On the face of it, perhaps this seems a more nurturing approach, although according to Cabañero, Eatable Adventures isn’t all that different from other investors. “We work at an early stage and some KPIs, such as revenue or market share, are less relevant,” he continues. “We normally look for a strong market-fit potential, a solid and ambitious team and, of course, strong IP or technology.”

.png)

Portfolio partners

Eatable Adventures works with a brilliant portfolio of start-ups that have gone on to become leaders in their respective market segments. As you can read in our article on bioprinting, Cocuus is already disrupting the plant and cell-based animal protein category. “It’s truly magic,” says Cabañero of the company’s technology. “Their 3D printers and bio-inks can really replicate popular meat and fish cuts, resembling the original and with a highly nutritious profile. It is not just in demo mode – its first large-scale bioprinters are already in late tests, demonstrating how it will churn out millions of kilos of alternative proteins a year.”

The biggest risk – and it’s a big one – is technology failure

MOA foodtech probably needs no introduction and combines biotechnology and AI to convert waste and by-products from the agri-food industry into what Cabañero describes as a “next-generation” protein. “It has a high nutritional value and is 100% sustainable,” he explains. Innomy, meanwhile, is basing its product on mycelium. “This is one of the most promising sources of protein for the future. The fact that fungi do not produce cholesterol or significant amounts of saturated fats has redirected the attention of the food industry toward them.”

After the boom for alt proteins in 2021, Cabañero is expecting a drop-off in 2022 from those record levels of last year. “We are still one quarter away from the end of the year, but so far we see a strong reduction in the plant-based segment, albeit cellular agriculture and precision fermentation seem to be holding firm.”

And despite continuing obstacles around regulations, consumer acceptance is still the main hurdle for the industry to overcome for Cabañero. “Producers still have some challenges to achieve taste, texture, and price parity with conventional proteins. This is why it is key to connect start-ups with the food industry to enable alternative proteins to scale up production to industry levels.”

Impact food-tech solutions are the catalyst for change

Although food-tech investments in 2022 have dropped on 2021 levels, early figures would appear to indicate, they haven’t suffered as badly as other sectors, such as digital solutions and fintech, according to Jaime Betech, Investment Associate at Good Seed Ventures. The fall, he suggests, could be attributable to the imminent recession in Europe and other countries around the world, while interest rate hikes have a direct effect on riskier early-stage investments. “We are looking at solutions that take significant resources to develop, produce and scale, which means that returns for investors may take longer to appear,” he says.

The gas crisis in Europe hasn’t helped either, which has raised the price of fertilizer that is used to grow many ingredients employed in food production. “The cost of energy continues to rise, and many start-ups require a lot of it to develop their solutions,” Betech continues. “Distribution and delivery of products has also become more expensive due to the ripples of the supply chain crisis.”

The company needs to be backed by hungry entrepreneurs that are motivated by the greater mission that their company is trying to solve

Rising above the challenges

Such factors notwithstanding, Betech is convinced the food-tech industry has the potential to overcome the crisis much better than other industries. “The solutions being developed not only help to feed a growing population but are aligned with the United Nations’ Sustainable Development Goals and various countries’ sustainability plans,” he says. “Price parity is on the horizon and consumer awareness toward sustainably sourced products continues to expand. This, tied to a growing demand for alternative proteins, makes it a compelling case.”

Good Seed Ventures boasts an impressive portfolio of food-tech entrepreneurs, including but not limited to Planted, Vly Foods, Formo, Meatable, Perfeggt and Supermeat. “When it comes to technology, we try to find start-ups with a roadmap for technological innovation as a driver for industry-transforming change,” Betech says, when asked what Good Seed Ventures looks for in a start-up. “The company needs to be backed by hungry entrepreneurs that are motivated by the greater mission that their company is trying to solve.”

Their solutions also need to be scalable at a global level, too, which means “ensuring the availability of ingredients, having freedom to operate in case of registering intellectual property, potentially co-manufacturing product to avoid excessive capital expenditure, and high levels of vertical integration along the value chain”.

Betech reveals a second pre-cursor for making it into Good Seed Ventures’ lineup. “You have to look at impact – we place this on a par with financial return,” he stresses. “Food-tech solutions are a catalyst for change when it comes to fighting global warming. We only partner with start-ups that have the potential to reduce at least 200,000 tons of C02e every year, 10 years after our initial investment. We are convinced that the next wave of unicorns will be the ones developing solutions that have the potential to stop climate change on a global level.”

An animal-based food supply system that is ripe for disruption

Elysabeth Alfano is possibly one of the most recognizable faces in the global alternative proteins sector. In addition to her business interests, she is also the host of the Plantbased Business Hour, created because she felt targeted plant-based business and innovation news was missing in the mainstream media. If there’s anyone more passionate than Alfano about this sector succeeding, we are yet to find them.

As the CEO of VegTech Investor, advisor to the world’s only Plant-based Innovation & Climate Exchange Traded Fund, her focus is on companies that can “scale large enough to trade publicly”. Consequently, Alfano certainly has (and needs to have) her finger on the pulse and when asked to identify some of the factors driving interest in alt proteins, she doesn’t hesitate in reeling off a whole list. “Political unrest driven by food insecurity and rising tensions in diplomatic relations will drive shorter supply chains and put a focus on creating alternative proteins and vegetables in controlled scenarios such as vertical farms and cultivated meat lab,” she says. The environmental crisis, climate change and water shortages will also drive the market. “Lastly,” Alfano adds, “profits will drive this market as the current system is wasteful and inefficient with resources and food will be made cheaper with higher profit margins.”

Educational policy

With VegTech Invest, Alfano has set out to educate the financial community about the societal and monetary benefits of investing in plant-based innovation and alternative proteins. “We are developing an educated and receptive public market for plant-based and alternative protein IPOs,” she reveals.

And it comes as no surprise to hear she believes the sector will achieve its ambitions, which for her have a much wider societal and planetary impact. “Ultimately, consumers want options,” she says. “I see all alternative proteins scaling – plant-based, fermented precision and biomass proteins, and cultivated meat (in that order) – to eventually replace animal proteins. This will happen because our current animal-based food supply system is ripe for disruption. These replacements to animal analogs have a smaller carbon footprint, save on resources like land and water, have the capacity to feed more people faster and more nutritiously, and even cut down on healthcare costs. These foods – and the companies that make them – provide solutions to critical problems.”

The true opportunity comes in making the increasing number of plant-based innovation and alternative protein start-ups robust enough to weather the venture capital storm

Speaking from a financial perspective, she feels the markets (and consumers) also “love” efficient solutions. “Provided,” she stresses, “these food solutions can compare on taste, price and convenience, people are willing to buy them. Thus, the true opportunity comes in making the increasing number of plant-based innovation and alternative protein start-ups robust enough to weather the venture capital storm. By growing large enough to IPO on the public markets, these companies can efficiently solve some of the world’s most pressing issues, at scale, and produce quantities [of protein] meaningful enough to shift the global food supply system to be more sustainable.”

Plant-based innovation companies such as Beyond Meat (an EATV holding) are already achieving this feat. “The company has manufacturing in China and Europe,” Alfano notes. “On the other end of the spectrum, cultivated meat still has a way to go for global regulatory approval and mass production potential. However, innovations such as cultivated meat fat – which is further along than cultivated meat – can help augment the taste profile of plant-based meats while allowing the base product to be primarily from plants.”

Supportive technologies such as cultivated animal fat and precision fermented animal casein are very interesting cases for Alfano. “I believe they can help existing plant-based companies scale faster and stronger with novel products that are tasty and familiar, but efficient and sustainable,” she says. “These ingredients technologies will allow the consumer to have even more options that fit their needs at the grocery store in the short term while positively impacting the planet and personal health.”

Alfano doesn’t need much pushing to predict how the sector will evolve, with globally recognized brands increasingly making their presence felt. “Not only will they begin to buy up plant-based companies, the world’s major food brands will put their distribution channels and advertising dollars toward plant-based production. Adoption and change will begin to happen really quickly.”

Addressing our food system’s most fundamental root cause problems

Therése Dalebrant is Head of Strategy & Investment Manager at Sweden’s Gullspång Re:food. When evaluating the credentials of a potential investment, Dalebrant and her colleagues always question whether a company seeking investment addresses a critical root cause problem in the food system. Does it have a clear strategy for overcoming the barriers to transformative change? And, importantly, might their solution have any unintended adverse side effects in society when scaled?

“We spend considerable time doing our homework,” she reports. “We have a good relationship with the Stockholm Resilience Centre and other researchers, which help us understand the food system, its hidden connections, and the most potent leverage points for change.”

The rest of the screening process is not too dissimilar to other VC firms though. “How big is the market? How much confidence do we have in the team, and how good is the fit with our strengths? Is the valuation of the company fair, given risks and potential returns? We invest as much time as we can in getting to know the founders – after all, we’re entering into a relationship that we hope will last many years.”

Two things distinguish Gullspång Re:food in the VC community, according to Dalebrant. “Our evergreen structure and our systems thinking approach,” she says. “Combined, these allow us to be a long-term investor backing companies that are addressing our food system’s most fundamental root cause problems – as opposed to the indirect symptoms caused by them.”

Transforming a system as complex and large as food takes time, and solutions with short-term effects often tend to improve the problem instead of eliminating or reversing its underlying root cause. “Our evergreen structure makes it possible to back long-term solutions as we don’t need to have any arbitrary exit timelines guiding our investment decisions,” Dalebrand explains. “We also tend to make fewer new investments in terms of the number of companies compared to traditional VCs. Instead, we prioritize more follow-ons for our existing portfolio.”

Meat-lovers will still be able to enjoy real meat, just grown more sustainably in cultivators as opposed to factory farms

Oatly happens to be a Gullspång Re:food portfolio company and Dalebrant reveals the alternative dairy leader is on track to generate more than US$800 million in revenue in 2022. “But this is very small compared to the overall potential,” she says.

No doubt about it, the alternative proteins sector is big business and based on data from Future Market Insights could be worth a total of US$500 billion for the decade between 2022-2032. Do these projections stack up in Dalebrand’s eyes? “It’s challenging to make such predictions,” she admits. “For two reasons, we believe the market for alternative proteins (and fats) will be huge. First, everyone must eat daily while the population grows, meaning we’ll need more proteins and fats. And second, animal factory farms are not sustainable and sooner or later regulations, competition (or both) will drive them out of business. Instead of predicting future growth, though, we try to accelerate it by finding and funding companies we believe can bring better alternatives at scale.”

Food security

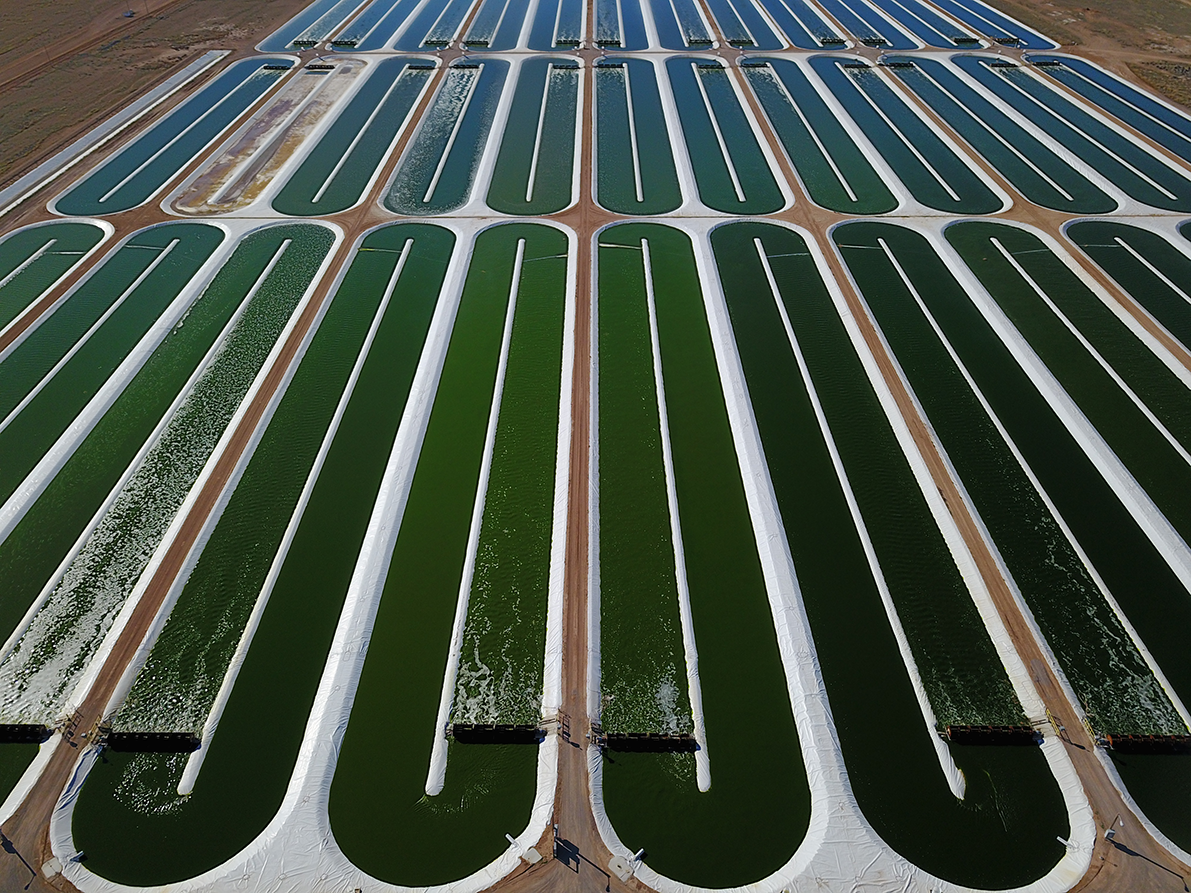

Ultimately, Dalebrant believes alternative proteins will play a fundamental role for future food security due to their resource efficiency over conventional meat and dairy. “We simply don’t have enough natural resources to sustain traditional livestock and dairy farming at scale as the population grows,” she says. “Alternative proteins can also provide much-needed replacements to conventional farming for areas without access to arable land or freshwater.”

An example here is the Gullspång Re:food portfolio company, iWi, which operates open-pond algae farms in the deserts of New Mexico and Texas where conventional farming is deemed impossible. “Their algae production yields almost 6,000 lbs of amino acids per acre using absolutely no freshwater. In contrast, pea protein – which is widely regarded as a resource-efficient crop – yields around 20 lbs of amino acids per acre using almost 9,000 gallons of freshwater per pound,” she explains.

“Over the next few years, several functional ingredients used in food typically sourced from animals can be replaced using precision fermentation or cell cultivation. These ingredients ranging from animal-based fat to collagen, gelatin, and casein, will drastically improve the taste, texture, and nutritional quality of today’s alternative protein products.

"Over the next decade, there will be more options beyond just plant-based proteins, catering to various consumer preferences. Meat-lovers will still be able to enjoy real meat, but it will just be grown more sustainably in cultivators as opposed to factory farms. Vegans will enjoy the improved taste, texture, and nutritional quality of plant-based products. We also believe that grass-fed animals will play an essential role in a sustainable food system, but at significantly lower volumes and in better living conditions. Game meat will also be a sustainable source of protein in the future.”

Paying close attention to the wants and needs of the people they are trying to serve

“Our many years of working with founders have taught us that simply providing funding is not enough to help companies level-up,” insists Manav Gupta, Founder & CEO of Brinc. “Beyond capital, many founders come to us with challenges ranging from technical validation to go-to-market strategies,” he continues. “Particularly in a novel space like alternative proteins, getting access to a network of founders, mentors, and industry experts is becoming increasingly important to help companies move toward commercialization. As a global venture accelerator, we take an active role in helping early-stage start-ups to improve by providing access to not only funding, but also mentorship, investor networks, technical support, and more.”

As Asia’s first food technology accelerator, Brinc has supported more than 50 start-ups in their mission to improve our food system over the past three years. “Beyond access to the Asian ecosystem, the depth and diversity of our portfolio companies give founders an opportunity to partner with and learn from each other,” Gupta explains. “Alumni of our programs will frequently return to speak with our newest cohorts, sharing insights from when they were building at an early stage and their journeys beyond.”

Support network

Although Brinc is investing in start-ups, Gupta says his company’s role is to get behind the founders, the primary driving force of early-stage start-up success. “When looking at a company, we place a lot of emphasis on the founding team, in particular their ability, and any previous track record, in bringing a product to market. We typically look for co-founder teams where there is more than one founder running the company.”

Beyond the team, Gupta says Brinc also focuses greatly on how defensible the technology of the product is. “This could look like having strong IP for the technology used to create the end-product,” he reveals. “In the current investment climate and increasingly competitive alternative proteins space, it is no longer enough to simply want to create the next plant-based or cell-based burger – we need to start looking at truly disruptive technologies that are scalable and able to improve the cost and production efficiency of alternative proteins.”

In the current investment climate and increasingly competitive alternative proteins space, it is no longer enough to simply want to create the next plant-based or cell-based burger

Finally, Gupta notes, he and his team also pay close attention to how ‘tapped in’ start-ups are with their target demographics. “Particularly in plant-based products, key indicators that investors pay attention to include customer retention and product market fit,” he explains. “This could come in the form of initial revenue from market launches, or, at the early stage, data from consumer taste tests that signal a product is not a ‘one-time’ purchase, but something that will benefit from repeat business. Foremost, we want to see that start-ups are paying close attention to the wants and needs of the people they are trying to serve.”

Success in the food-tech space is also about partnerships and getting in touch with the right people. From letters of intent for distribution partnerships to pilot agreements with corporates, Gupta says he gets excited when start-ups come to Brinc with interest built from potential customers.

“We don’t expect teams to have all of the above,” he notes. “We are excited to keep helping game-changing start-ups become commercially plugged-in and institutionally investor-ready throughout and after our accelerator programs.”

Although Gupta doesn’t want to pinpoint any one portfolio company in particular, he finds it hard not to give some kudos to Orbillion Bio. The company, led by Patricia Bubner, Founder & CEO, has built key scale-up innovations, forming proprietary platform technology to rapidly decrease the cost of cultivated meat by 10x, as well as speed up the process by 18x – two of the biggest pain points in the cell-based meat space. “Orbillion’s first products will be focused on premium, heritage varieties such as wagyu and bison,” reveals Gupta.

He also reserves a special mention for Sophie’s Bionutrients. “They are developing a new plant-based protein out of microalgae using fermentation technologies,” says Gupta. “They are solving the looming protein shortage issue with their patent-pending sustainable protein production technology.”

Collaboration is key in overcoming the challenges facing all industry partners

Although there are rewards from investing in alternative proteins, there are also risks, especially in the uncertain marketplace we are seeing today. There are four critical challenges facing not just investors but the whole sector: scalability and raw materials; regulations; consumer acceptance; and, finally, IP and technology.

Juliette Raoul-Fortésa, a Venture Capital Analyst at Capagro, doesn’t believe these are insurmountable challenges, but they cannot be solved overnight. “Scaling capacity is an issue for most of this space’s start-ups,” she concedes. “And within each of the different areas – plant-based, fermentation and cell ag – we see even more specific challenges.

“For plant-based products, these include the optimization of protein crops, the availability of said proteins and of needed ingredients to obtain tasty and textured products at a reasonable price, and a short list of ingredients to become clean-labeled.

“With fermentation, there are challenges around increasing metabolic efficiency, avoiding GMO cells, adopting low-cost feed-stocks and optimizing the downstream process (which is currently tremendously costly), not forgetting the availability of fermenters.

“In cell ag, there are hurdles around avoiding GMO cells, reducing media cost, and suppressing Fetal Bovine Serum (which isn’t at all vegan).”

We really don’t see ourselves as just financial players, but strategic partners that can help start-ups thrive and scale

To a certain extent, Raoul-Fortésa feels, the plant-based sector is rather spared when it comes to regulations, certainly in comparison to fermentation or cell ag. “It might be easier for precision fermentation to be compliant as this technology is already used in the pharma space, so a regulatory framework exists,” she notes. “There is hope regarding the other technologies as there have been various recent advances, such as sales in Singapore, samples authorized in the Netherlands, and President Biden’s recent apparent affirmation of the use of biotechnology in foods.”

Prequisites

In terms of consumer acceptance, Raoul-Fortésa suggests the challenge for start-ups is to target the flexitarian market and to educate its potential clients, especially for fermentation and cell ag.

“We definitely want to target companies that present a unique technological advance,” Raoul-Fortésa says. “We realized that many start-ups have pending patents, and very few seem to be granted, so we hope there won’t be too much of an overlap.”

Apart from the fact that Capagro can financially accompany its portfolio companies on the long run, its independent AgriFoodTech fund is quite unique in the sense that it has gathered a set of limited partners (LPs) from within the whole agrifood value chain – agricultural cooperatives, food industrials, financial actors, etc. “They advise us on various subjects (tech matters, industrial, market insights, etc) and we create as many synergies with them as we can between our portfolio and deal-flow companies (business, R&D, industrial, commercial). We are also quite connected to the start-up space and have close relationships with various accelerators, incubators, and VCs, which benefits our portfolio companies. We really don’t see ourselves as just financial players but strategic partners that can help start-ups thrive and scale.”

Raoul-Fortésa highlights Capagro’s French portfolio company, La Vie, as one to watch. “They produce vegan sliced and diced bacon based on a proprietary technology, from which it produces the very first vegan fat that mimics animal fat characteristics during cooking, so no more compromises on taste and texture,” she says. “This enables the bacon to sizzle in the pan while the fat remains in place, without melting. They really have cracked the code and manage to sell those products at a competitive price compared to conventional animal-based products. It even generates 88% less CO2 than regular bacon and uses 82% less water and 74% less land.”

Investment capital will, in the future, be more selective and expensive

Nobody knows for certain where the industry will be in 10 years’ time, suggests Brian Ruszczyk when asked about recent market forecast predictions of a US$500 billion alternative proteins market over the course of the next decade. “But what we do know is that, in 2022, the industry flatlined in growth and revenue due to a variety of extraneous factors and most likely temporary events, such as inflation, war, supply chain breakdowns, etc. However, we believe the industry will recover and continue its upward trajectory from its current smaller base over the years.”

With predictions from think tanks and entrepreneurs alike, the Co-founder & CEO of Earth Food First Ventures (EFFV) usually prefers to slash those estimates by half for a “reality check”. A more realistic outlook such as this would still value the alternative proteins market at a more conservative US$250 billion in top-line revenue by 2032, which, as Ruszczyk notes, is “still a respectable 10x growth from current levels”.

Although a glass-half-full kinda guy, Ruszczyk believes the whole ecosystem for alt-proteins has taken a step back in 2022, whether due to market turmoil, the war in Ukraine, uncertainty around the food supply chain collapsing, bond and equity markets, or soaring inflation and tighter monetary policy worldwide. “Valuations were out of whack in 2020 and 2021, and some investors in this space were tipping the scale into absurdity and are now having to deal with US$100 billion in write-offs,” he says.

He thinks more reasonable valuations have prevailed in 2022 – for those that found funding – but for sure, the amount of abundant capital put to work in the sector will not equal anywhere near what occurred in 2021. “Investment capital will be more selective and expensive,” believes Ruszczyk. “We anticipate multiple failures, consolidations and reshaping of the landscape in alternative proteins. As capital regroups so, too, must the industry reshape itself.”

Plant-based products have become saturated and need to get to price parity to achieve anything meaningful and mass market

Turn up the volume

From Ruszczyk’s perspective, the biggest risk and challenge to the industry is the lack of infrastructure and commercial capacity to produce anywhere near the volume of alternative proteins many companies are claiming they will achieve in their five-year business plans. “We need vast amounts of capital to move into infrastructure, facilities, bioreactors, and extruders for the industry to scale – this will not be done exclusively with traditional VC capital. Novel protein producers and infrastructure providers will need to access a wider pool of capital, including debt, government, and long-term institutional funds.”

In looking at the markets today, Ruszczyk feels the current economic environment and market turmoil are already taking their toll. “We are in a risk-off market in the public markets from bonds to equity,” he says. “Private markets and venture will be no different – risk-off is risk-off. As with all market corrections this, too, will pass and capital will begin to flow again when the Fed has finished its tightening, inflation falls back to normalized levels, and the war in Ukraine is resolved. Our take is that we are probably in for a rough ride for the next two years and, by definition, this will stimy progress in the alternative proteins space. But this translates to huge opportunities for us to back winners in alternative proteins at reasonable valuations in a difficult market.”

So, what is Ruszczyk’s view of the significant correction in the shares of certain plant-based companies vis-à-vis the future of plant-based products? “The plant-based meat industry has not failed at all,” he adamantly says. “Some public stocks have plummeted because they were priced like Tesla and are now properly priced like Kraft Heinz.”

Recent articles have pointed out the correction in the share valuations of the few listed plant-based companies. For example, in the case of Beyond Meat, its stock went from US$10 billion to US$1 billion, and the media quite rightly pointed that out, but, observes Ruszczyk, “over the past 10 years, Beyond has grown its revenues from US$50 million (when it went public) to US$600 million today”.

And he notes the plant-based industry overall has grown from near zero to US$20 billion in top line revenue. “Plant-based products,” he offers, “have become saturated and need to get to price parity to achieve anything meaningful and mass market”. But, at the end of the day, if the consumer doesn’t buy in, it’s not going to fly – and, at the moment, the consumer is still demanding meat regardless of planetary destruction. “Consumer education is a key component for the overall commercial success of plant-based and the larger alternative protein markets. I view this as another hiccup in a long journey toward greater market share – maybe not 20% but certainly 10% over next decade or more as products improve and prices drop. But that is certainly no easy task.”

The tailwinds that have propelled the market still exist

“Venture capitalists always build out a balanced portfolio of investments because not all of the investments will be successful,” reports Hendrik Van Asbroeck, Partner at Astanor Ventures. “This doesn’t mean we are investing carelessly, hoping that some of it will take off. Rather, we have built a thoughtful process to fully support the entrepreneurs we have selected.”

The Astanor team has a very solid background in investing and in accompanying companies across their operations. “We are active investors,” reveals Van Asbroeck. “We tend to lead an investment round where possible and hold a board seat to help guide the company’s growth,” he says. “We work closely with management in making strategic decisions for the firm including business development, capex investments, go-to-market strategy, financial decisions and HR (helping to build out the best team).”

Astanor also makes its network accessible for its portfolio companies, which can help commercially, financially and strategically. “We have a worldwide network of food experts, such as chefs, nutrition, food, agriculture and biotech,” Van Asbroeck says. “Our advisors have first-hand experience on the field and can provide the most relevant insights. We focus mainly on impact and ESG, helping companies grow sustainably while maximizing their impact.”

So, what is Van Asbroeck’s take on 2022 so far, after a few very, very successful years for the alternative proteins market? After “accelerated growth” for alternative proteins during the Covid years, “driven by animal protein shortages” and “curiosity about a new and interesting product”, he sees that there has been some “year-over-year shrinking” in the marketplace. “There were many new start-up brands in the space and some consolidation and contraction of brands is to be expected,” he says. “And some of the market leaders may have expanded too fast and then decided to downsize their staff.”

On a positive note, though, the broad trend, as measured by five-year CAGR, shows steady growth. “The tailwinds propelling this market – government regulations of industrial animal production, consumer search for healthier ingredients, advances in making alternative proteins that are affordable and tasty – continue to exist and grow,” Van Asbroeck highlights.

We have built a thoughtful process to fully support the entrepreneurs we have selected

According to the Astanor chief, the plant-based protein market today is worth roughly US$12.2 billion. “We have no doubt the market will continue to grow,” he says. After all, meat, seafood and dairy are a huge part of the global diet, and a significant chunk of that current market is available to alternative protein companies to grab. Overall, protein worldwide is valued at more than a trillion dollars, so even 10-20% of that is quite impressive and will have a significant impact. This context also provides sufficient growth potential for venture capital investors – such as Astanor Ventures – to invest in and support “promising actors” of the alternative proteins market.

Big impact

One of the biggest challenges for Van Asbroeck and his team, though, is adoption rate. “To have real impact, you need to be able to convince the general public to eat alternative proteins on a regular basis,” he says. “Alternative protein brands shouldn’t only focus on the already convinced group of people (e.g. the 100% vegetarians) but should help foster the habit of consuming alternative proteins, making it part of a common diet.”

Another issue is how to approach the alternative proteins market. How do new entrants position themselves? Van Asbroek suggests they need to figure out how to work with the industry, if they can use existing channels, and whether they should build a new brand or not.

According to Van Asbroeck, it is also important to evaluate the life-cycle assessment of a product. “Companies should ensure they have a view of their full value chain and that they understand how sustainable their product and offer is,” he advises.

It is also vital that alt protein companies focus on the digestibility and health attributes of their products. They should have a positive impact on consumers’ health. Which added value are they bringing to the table? Is their product healthier than other options? Further, he adds, it is key to assess potential health risks (additives, fat, etc) that could hurt the sector in the long run.

And, as we constantly hear, another sizeable hurdle to overcome is taste. “Consumers mostly choose their products based on price and taste,” Van Asbroeck concludes. “They are attentive to the flavor and texture of ingredients. However, alternative proteins are often quite bland, or have strong flavors that consumers aren’t looking for (bitter, bland, woody, etc). Texture is often not the moist, toothsome texture people are used to – instead it’s too fibrous or tough. So, many alternative protein brands are still trying to get the taste right to gain consumers’ approval.”

Alternative proteins and the push for greater sustainability and shorter, more resilient supply chains

“By 2035, every tenth portion of meat, eggs and dairy eaten around the world is likely to be alternative,” believes Björn Witte, Managing Partner & CEO of Blue Horizon, referring to research conducted alongside Boston Consulting Group a year ago. “This would represent a global market of US$290 billion.”

Regardless of the economic estimates, Witte believes consumers around the world want healthier foods – both for themselves and the planet. “We recently conducted a survey where we found that more than 30% would fully switch their diets to alternative proteins if doing so would have a major impact on climate,” he continues. “Consumers want to see continued improvements in health, taste, and price. The share of consumers eating only or mostly alternative proteins would double if their main inhibitors were overcome, the most frequently mentioned of which include health and nutrition, taste and safety.”

Resilience to supply chain shocks

This is why Witte is not overly concerned with the economic pullback we have seen in 2022. “It has affected all types of companies, from software to synthetic biology,” he says. “Alternative protein companies are not immune from such broad trends, but the transformation toward a sustainable food system is underpinned by strong secular drivers, such as the push for greater sustainability and shorter, more resilient supply chains.”

With alternative protein supply chains often being shorter and more resilient than conventional animal protein production, some governments are already taking steps to invite infrastructure and technology players (companies building bioreactors for cell-based proteins) into their jurisdictions, pushing development of local economic clusters around alternative protein capabilities. “So, in the end,” Witte states, “the current global economic climate only supports the transition to a more sustainable food system as it accentuates the need for a change for many countries around the world.”

Blue Horizon is not only active in the venture capital space, Witte notes. It takes a “full life-cycle approach” to the companies it invests in, with the “resources and conviction to support founders’ progression from idea to exit”.

Issues such as global food security and sustainability across the value chain are finally on the frontpage of the newspapers

The firm has been active in the alternative proteins market since 2016 and has now made investments in more than 70 alternative protein and food-tech companies. “We were an early investor in several companies that have since become unicorns such as Beyond Meat, Impossible Foods and EAT Just,” Witte reveals. “The ecosystem we have built gives us access to deals many others are denied to. A second factor for our success is our team. We have, just over the past 24 months, been able to add high-caliber professionals to the team and have now grown to more than 30 employees. An additional differentiator is the fact that the Blue Horizon team now includes academics, industry veterans and traditional finance experts. This mix allows us not only to analyze the market, but to truly understand it down to the last detail.”

Given this font of knowledge, when asked about technology trends, Witte is convinced cultivated meat will become a vital part of the mix. “Many new start-ups are dabbling in the area, which has led to healthy competition and encouraged further innovation,” he says. “One of our portfolio companies, Mosa Meat, recently made international headlines when Leonardo DiCaprio invested in the company. Mosa Meat also announced a few months ago that it was able to reduce the cost of its growth medium, which is needed to grow cells in the bioreactor, by a factor of 66. As Mosa Meat continues to lower production costs, this will ultimately lead to the scalability of a new product on a global scale.”

Another Blue Horizon portfolio company is SuperMeat, which last year introduced the world’s first commercial platform for farmed chicken called ‘The Chicken’. “Today, as a consumer, you can dine at The Chicken and at the same time take a look at SuperMeat’s factory, where you can see how your chicken burgers are made under the same roof.”

Another highlight is Arkeon, an Austrian company producing proteins from carbon dioxide. “Arkeon converts CO2 directly into all 20 amino acids that are essential for human nutrition,” Witte says. “At the same time, this opens up a whole new world of food.

Ultimately, Witte thinks the alternative proteins space has benefited from the more recent geopolitical developments. “Issues such as global food security and sustainability across the value chain are finally on the frontpage of the newspapers,” he says. “It is tragic that it takes an extreme crisis for people to really wake up, but this is now happening, and this offers all of us the opportunity to really make a difference.

“Food is the biggest industry on our planet, and if we can leverage this and accelerate the shift to a more sustainable system, then we have a real chance of getting our future back on the right track.”

Investing in companies working to solve key challenges in the alternative protein industry

“When you are trying to prove a segment and grow penetration and your hero SKUs fall short on taste, it’s the entire product category that suffers,” believes Andrew D. Ive, Founder & Managing General Partner at Big Idea Ventures. “We face risks if the industry at large keeps investing in products that aren’t delivering on taste.”

The key to perfecting taste, according to Ive, lies in innovation. “We need to invest in companies that are developing scaffolding or ingredients solutions or perfecting texturization, and reducing the reliance on single plant-based proteins – not just in products that have been created just to fill a gap in an established brand’s product range.”

Thankfully, Ive notes, there are plenty of young companies working on exactly these kinds of solutions and the investors who are well versed in the industry support them. “The ecosystem is learning from its mistakes and growing stronger than ever,” he confirms.

“One of the things we look for in founding teams is determination and an unwillingness to quit,” Ive explains. “What we have seen is that team members who are committed, who grind through the challenges, and who have a passion for what they’re doing, have better chances of success. Another aspect is how the founders are able to translate their vision into something consumers or their target audiences want and need. If they are smart, they engage with as many potential clients or consumers as possible, and really listen to them.”

Ive thinks many of the factors driving the market in alternative proteins are mirrored in Big Idea Ventures’ portfolio. “Our initial cohorts had a lot more CPG and plant-based companies,” he recalls. “Our recent accelerator cohort is almost entirely B2B with companies working to solve the industry’s key challenges. These include new extraction and fermentation methods, AI-enabled micro fluids, connected bioreactors, cell-based fats, etc. When we invest today, we look for companies that have the basic skeleton of a solution, and who can go sell it to everyone in the industry. A lot of them can also customize their solution to each customer in the market, which is how they maximize revenue.”

Ive also advises that we should keep in mind the nuances between different continents. The key drivers in some parts of the world are certainly concerns about sustainability and climate change and in other parts of the world, a desire for more protein at a price that can be achieved with a small income. “Macro considerations are often only considered when our basic needs are met,” says Ive. “If we want to achieve our sustainability goals, we must also meet the basic needs of our people for good-quality protein at an achievable price – thankfully the technologies we’re developing are more cost efficient at scale.”

The next wave of alternative meat products are likely to combine textured vegetable protein with cell-based fats

Opinions of difference

As an investor, Big Idea Ventures is “unique in a few different ways”, Ive suggests. “With our New Protein Fund, we have a singular focus on the alternative protein industry. This gives us an edge in that we have a much deeper and thorough understanding of the ecosystem, and an unrivaled network of partners. It makes our accelerator program more relevant for our founders and our investments more attuned to market needs. Our program itself, which is now in its sixth cohort and has supported 87 companies, gives us insights into the latest innovations and technologies on the market. We know what works and what doesn’t earlier than anyone else in the industry. We can see patterns, make connections, induce partnerships and just generally create more value for every member of our community, whether that’s an investor, a corporate leader, a founder or a mentor.”

Another difference for Ive revolves around mentorship. “We have four scientific fellows, including two PhD food scientists, who work closely with the companies on their recipes, ingredients, production methods, etc. We also have a very close relationship with our limited partners and their in-house experts who truly understand how to not only innovate with food but ensure it is scalable.”

In a decade, Ive predicts we will produce proteins of all kinds using a combination of traditional animal protein, fermentation and cell-based methods. We will have the capability to create pork, beef, seafood, dairy and other protein types that will deliver on our taste, nutrition, and cost goals in a far more sustainable way than our current approaches. “Between now and then, we will see many incremental changes that will combines old and new technologies,” he says.

“The next wave of alternative meat products are also likely to combine textured vegetable protein with cell-based fats,” he concludes. “Getting fat right is important because it’s largely responsible for what will ‘feel’ like meat. And producing cell-based fats is much easier than producing muscle tissue, so these products are interesting because they are likely to address both the taste and texture challenge we currently face while keeping production cost and scalability in check.”

If you have any questions or would like to get in touch with us, please email info@futureofproteinproduction.com

More Features

Protein Pioneer: Justin Kolbeck

Deep Dive: Breakout bets

Feeding change

Protein Pioneer: Kesha Stickland